According to the Organisation for Economic Co-operation and Development (OECD), blue or marine biotechnology is “the application of science and technology to living organisms from marine resources, as well as parts, products and models thereof, to alter living or non-living materials for the production of knowledge, goods and services".[1] Blue biotechnology relies on biological material sourced from marine organism, such as algae, cyanobacteria, fishery by-products, microorganisms, etc., and represents a cross-cutting approach spanning multiple industries and applications. Unlike traditional seafood production, blue biotechnology creates higher-value products through advanced biotechnological processes, thereby generating economic value [2]. Some applications include pharmaceuticals, cosmetics, feed ingredients, biomaterials, and specialized chemicals. Its conceptual framework has evolved beyond resource exploitation to incorporate marine ecosystem restoration and health, reflecting growing awareness of ocean sustainability challenges.[3]

The potential for growth of the industry, both in Europe and worldwide, is significant due to several factors:

- Rich marine biodiversity: Europe has extensive coastlines and access to diverse marine ecosystems, offering a wide array of marine organisms that can be utilised for biotechnological applications.

- Increasing demand for sustainable resources: with growing concerns over sustainability and environmental degradation, there is a rising demand for alternative and sustainable sources of raw materials.

- Technological advancements: advances in biotechnology, genomics, and bioinformatics have enhanced our ability to explore and exploit marine organisms for various applications. These technological advancements enable the discovery of novel bioactive compounds and the development of innovative bioprocessing techniques.

- Economic potential: the commercialisation of products derived from marine organisms can create new economic opportunities. As notable applications include, Several blue biotechnology products may have extremely high value added (e.g. anti-cancer drugs, anti-inflammatory compounds, nutraceuticals and cosmetics).

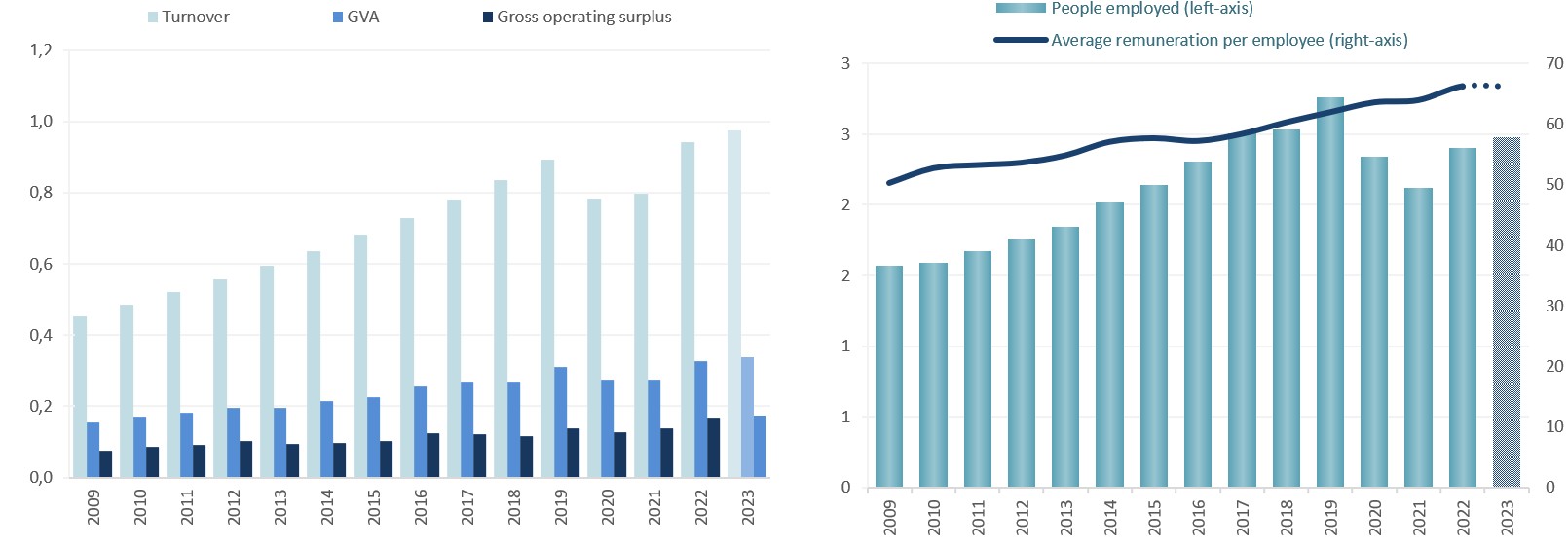

The sector generated a GVA of EUR 327 million in 2022, a 19% increase compared to 2021. Gross profit, at EUR 168 million, increased by 21% compared to the previous year. The turnover reported for 2022 was EUR 942 million, an 18% increase on the previous year.

Estimates for 2023 suggest an increase of around 3% for GVA, turnover and gross profit.

In 2022, roughly 2 400 persons were directly employed in the sector, 13% more than in 2021. The annual average wage was estimated at EUR 66 300, up 4% compared to 2021.

Whilst it is estimated that the average remuneration will stay similar in 2023, an increase by 3% in the employment is foreseen for the industry for the same year.

Germany leads employment within Blue biotechnology, contributing with 18% of the jobs and 29% of the GVA, followed by France (18% of jobs and 21% of GVA), Italy (11% of jobs and 11% of GVA), Spain and the Netherlands (both accounting for 9% of jobs and 7% of GVA).

Trends and drivers

From 2000 to 2023, the European blue biotechnology industry has attracted an increasing number of investments. Indeed, whilst between 2000 and 2018 the number of deals (i.e. investment agreements) closed was 90, from 2018 to 2023 the quantity increased to 114[4]. These deals amounted to EUR 405 million, with an average deal size per transaction of EUR 5.1 million and a median size of EUR 1.3 million, most often in the form of grants and early-stage investments[5].

The evolving needs of society as well as new lifestyles create a demand for diverse and nutritious food options, improved health and well-being, novel biomedicines, natural cosmeceuticals, environmental conservation, and sustainable energy sources[6]. Such demand is expected to fuel further research and development in the emerging field of blue biotechnology.

Marine organisms produce a wide range of bioactive compounds with potential pharmaceutical applications, including antimicrobial agents, anticancer drugs, and anti-inflammatory compounds. Exploiting these natural resources can lead to the discovery of new drugs and therapies.

- Marine-derived pharmaceuticals: marine organisms produce a vast array of bioactive compounds, many of which have demonstrated pharmacological properties. These compounds have the potential to be developed into novel drugs for various therapeutic applications, including antimicrobial, anticancer, anti-inflammatory, and antiviral agents. For example, seaweeds contain a large variety of phytochemical constituents that can be used in the prevention and treatment of health diseases.[7]

- Drug discovery and development: blue biotechnology offers opportunities for the discovery of new drug candidates through bioprospecting, screening natural products, and studying marine organisms’ unique biochemical pathways. With the increasing prevalence of drug-resistant pathogens and unmet medical needs, marine-derived therapeutics present promising avenues for drug development.

Marine-derived ingredients can be incorporated into functional foods and nutraceuticals, offering health benefits such as omega-3 fatty acids, antioxidants, and vitamins. The growing demand for natural and functional ingredients presents opportunities for the development of marine-based food and dietary supplements.

- Omega-3 fatty acids and essential nutrients: marine organisms such as fish, algae, and seaweeds are rich sources of omega-3 fatty acids, vitamins, minerals, and other essential nutrients beneficial for human health. These ingredients can be incorporated into functional foods, dietary supplements, and nutraceuticals targeting specific health conditions, such as cardiovascular disease, cognitive function, and immune support.

- Anti-oxidants and bioactive compounds: marine-derived antioxidants and bioactive compounds exhibit potential health benefits, including antioxidant, anti-inflammatory, and anti-aging properties. Incorporating these ingredients into food and beverage products can enhance their nutritional value and appeal to health-conscious consumers seeking natural and functional ingredients. Carotenoid pigments from brown algae for their antioxidant activity as well as positive health effects to treat obesity and type-2 diabetes[8].

Exploring marine biodiversity for biotechnological purposes can lead to the discovery of new species and genetic resources with potential commercial value. By promoting biodiversity conservation and sustainable use of marine resources, blue biotechnology contributes to the preservation of marine ecosystems.

- Discovery of novel species and genetic resources: marine ecosystems harbour a vast diversity of species, many of which remain unexplored and undocumented. Bioprospecting expeditions and genetic studies can lead to the discovery of new species, microbial strains, and genetic resources with potential biotechnological applications, including enzymes, bioactive compounds, and metabolic pathways.

- Biodiversity conservation and sustainable use: blue biotechnology promotes the sustainable utilisation of marine resources while conserving biodiversity and protecting fragile marine ecosystems. By adopting principles of responsible bioprospecting, ecosystem-based management, and Maritime Spatial Planning, stakeholders can balance economic development with environmental conservation, ensuring the long-term viability of marine biotechnology initiatives.

Marine microorganisms and algae can be used for the production of biofuels, such as biodiesel and bioethanol, as well as for bioremediation purposes to clean up marine pollution. These applications contribute to the development of sustainable energy sources and environmental conservation efforts.

- Biofuel production: Marine microorganisms, particularly algae, offer a promising source of biomass for biofuel production, including biodiesel, bioethanol, and biohydrogen. Algae cultivation can be conducted in various marine environments, including open ponds, photobioreactors, and offshore facilities, utilising sunlight and seawater to produce renewable energy resources.

- Bioremediation of marine pollution: marine microorganisms possess unique metabolic capabilities for degrading organic pollutants, such as hydrocarbons, heavy metals, and wastewater contaminants. Bioremediation technologies based on marine biotechnology can be applied to clean up oil spills, industrial wastewater, and marine debris, mitigating environmental pollution and restoring ecosystem health.

To find out more about what the Commission is doing to support the EU Algae sector, as well as to discover other infographics, please visit the AAM website.

Figure 1: Blue biotechnology market value by EU country, 2021

The pie chart illustrates the distribution of the blue biotechnology market value among EU countries in 2021 as broken down below:

- Total EU Market Value: €868 million in 2021, projected to grow to €1,786 million by 2032 at a compound annual growth rate (CAGR) of 6.8%.

- Germany: Accounting for 28% of the EU market, Germany's share equates to approximately €243 million. It's anticipated to experience a higher growth rate compared to other EU countries.

- France: Representing 23% of the market, France's share is about €200 million. Like Germany, France is expected to see accelerated growth in this sector.

- Other EU Countries: The remaining 49% of the market, totaling around €425 million, is distributed among other EU member states.

This distribution highlights that Germany and France together constitute slightly more than half of the EU's blue biotechnology market value. Both countries are projected to outpace others in market growth, underscoring their significant roles in this sector.

Figure 2: Blue biotechnology market value by application, 2021

The pie chart illustrates the distribution of the blue biotechnology market value by application within the European Union (EU) for the year 2021. Detailed below:

- Drug Discovery: This segment constitutes the largest portion, accounting for 24% of the market. This reflects the significant role of marine-derived compounds in developing new pharmaceuticals.

- Vaccine Development: Representing 13% of the market, this segment highlights the utilisation of marine biotechnology in creating vaccines. It's noteworthy that this area is projected to experience substantial growth, with an anticipated compound annual growth rate (CAGR) of 10.2% until 2032.

- Genomics: Also comprising 13% of the market, genomics involves studying the genetic material of marine organisms. This segment is expected to grow at a CAGR of 9.06% until 2032, indicating its increasing importance in the sector.

- Bioengineering: This application area accounts for another 13% of the market, focusing on applying engineering principles to marine biological systems.

- Other Applications: The remaining 37% of the market encompasses various other applications of blue biotechnology, including environmental management, biofuels, and food production.

These trends are consistent across all EU Member States and reflect a growing consumer interest in products derived from marine compounds. Additionally, pharmaceutical and medical applications tend to offer high added value, contributing to their prominence in the blue biotechnology market.

Blue biotechnology involves using marine resources to develop products and technologies across various industries, including pharmaceuticals, food, and environmental management. The projected growth in this sector reflects increasing investments and advancements in marine-based biotechnological research and applications within the EU.

Figure 3: Blue Biotech Funding by Segment (€ millions)

The bar chart illustrates the allocation of private funding within the European Union's blue biotechnology sector for the year 2023.

Total Private Funding: In 2023, the EU's blue biotechnology sector attracted approximately €184 million in private investments.

Seaweed and Algae Startups: A substantial majority of this funding, about 95%, was directed towards startups specialising in seaweed and algae. This equates to roughly €175 million.

This funding distribution underscores a significant investor interest in marine-based solutions, particularly those involving seaweed and algae, due to their versatile applications and potential for high returns. The focus on these areas reflects a broader commitment to sustainable and innovative practices within the EU's blue biotechnology sector.