xx

Desalination is the process of removing dissolved salts and impurities from saline water—such as seawater, brackish water, or mineralised groundwater—to produce water that meets specific quality standards for human consumption, irrigation, industrial applications, and other uses (Figure 1).

The freshwater output usually requires post-treatment – such as remineralisation and pH adjustment – to produce water that meets specific quality standards for human consumption, irrigation, industrial applications, and other uses, and to protect distribution systems from corrosion. The process generates a concentrated byproduct (brine), which must be managed properly to minimise environmental impacts.

Brine is the highly concentrated saltwater solution that remains after freshwater has been removed during desalination. It contains a very high level of dissolved salts – typically sodium chloride along with other minerals, in the same proportion as in source seawater – and may include residues of the flocculants and antiscalants used during pre-treatment or the desalination process.

Because brine is far saltier than the original feedwater, its disposal back into the sea – especially in large volumes and in presence of strong seafloor currents – can alter salinity, temperature, and chemical concentrations in the vicinity of the discharge point. Consequently, proper management of brine is essential in order to minimize impacts on marine ecosystems.

Desalination is one of the three pillars supporting water resilience globally, together with water use optimization (including reuse) and water storage (including provisioning and regulating ecosystem services). Its technological complexity and cost compared to conventional water resources have so far limited desalination to a “last resort” option when the other two pillars are insufficient.

Under climate change, we expect that many regions in the EU – especially, southern European Member States – and globally will face severe water scarcity[1], and the population currently exposed to severe water scarcity in Europe may rise from about 50 million at present, up to 65 million people under an increase of 3°C in global average temperature[2]. In this context, desalination may prove essential to ease pressure on water systems[3], [4]. In this scenario, with appropriate brine management and decarbonisation of its energy use, desalination may become a sustainable water management option suited for broad uptake[5].

Two main processes have been utilised to remove salt from water so far: thermal distillation and membrane processes. Thermal distillation processes work by applying heat to seawater or brackish water so that water evaporates and then is condensed as freshwater, leaving salts and impurities behind. In contrast, membrane processes use high pressures to force water through a semipermeable membrane that blocks salts and contaminants while letting purified water pass.

Because thermal distillation is more energy intensive, no significant projects using thermal desalination were developed in the last couple of decades, and few industrial players have remained on the market. Thermal plants remain as existing operating assets, but are poised to be gradually superseded, although they could be still suited in projects with zero liquid discharge (ZLD).

Membrane processes (specifically reverse osmosis, RO) consume less energy per cubic meter of water, are easier to scale, and have lower operating costs, although they need careful pre-treatment to minimize membrane fouling.

The main thermal distillation technologies employed for desalination include multi-stage flash distillation (MSF), multi-effect distillation (MED) with no vapour compression or with thermal or mechanical vapor compression (MED-TVC, MED-MVC). Among distillation technologies, MSF distillation accounts for the majority of installed global desalination capacity. It takes place in a series of chambers with successively lower temperatures and pressures. Saline feed water entering each stage chamber flashes to steam as the lower pressure causes boiling at lower temperatures, while heat exchangers condense pure water vapor from the steam. Recycling this latent heat of condensation improves thermal efficiency. MED also utilises multiple effects or stages but uses the heat from condensation of water vapour generated in one stage to pre-heat the feed water for the next stage. This cascade arrangement further improves energy efficiency. MED-TVC and MED-MVC allow further reducing energy input needs[6].

Because of its higher efficiency, RO has overtaken thermal processes to become the most widely used desalination technology globally. Typical RO systems use arrays of spiral-wound membranes or hollow-fiber membrane modules. Energy is needed to generate the required transmembrane pressure, which exceeds the naturally occurring osmotic pressure, to desalt the feed water[7].

Electrodialysis (ED) and electrodialysis reversal (EDR) use an electric potential applied across ion-exchange membranes to draw positively and negatively charged ions through selective membranes. This leaves desalinated water behind as the dilute[8]product. ED and EDR have found niche applications for brackish water desalination but have limited large-scale usage compared to RO.

Membrane technologies not yet proven at industrial scale include forward osmosis and membrane distillation (MD), which utilises low-grade heat to evaporate water across a hydrophobic microporous membrane. Hybrid thermal-membrane desalination processes that combine principles of distillation and membrane separation have also been deployed, e.g. in the MENA region, but the thermal component has proven costlier and less efficient compared to RO.

Global installed capacity for the production of desalinated water has increased significantly in recent years, at an average rate of about 7% per annum since 2010, corresponding to approx. 4.6 million m3/day yearly[9] In 2018, there were nearly 16 000 desalination plants worldwide[10], with a total global operating capacity of roughly 95.37 million m3/day (million litres/day)[11]. More recent studies estimate that there were more than 21 000 seawater desalination plants in 2022, with a daily global production of 99 million m3/day of desalinated water, but also more than 150 million m3/day of brine byproduct[12]. Currently, desalination is largely used in the Middle East and North Africa (MENA region) – accounting for 70% of global capacity – in the US, and only to a limited extent in Europe (about 10% of global capacity).

Although currently producing only a relatively small fraction of water resources, desalination is a rapidly emerging sector with a large potential in the EU. With climate change, it is expected that the EU desalination market will further expand in the coming years[13][14][15].

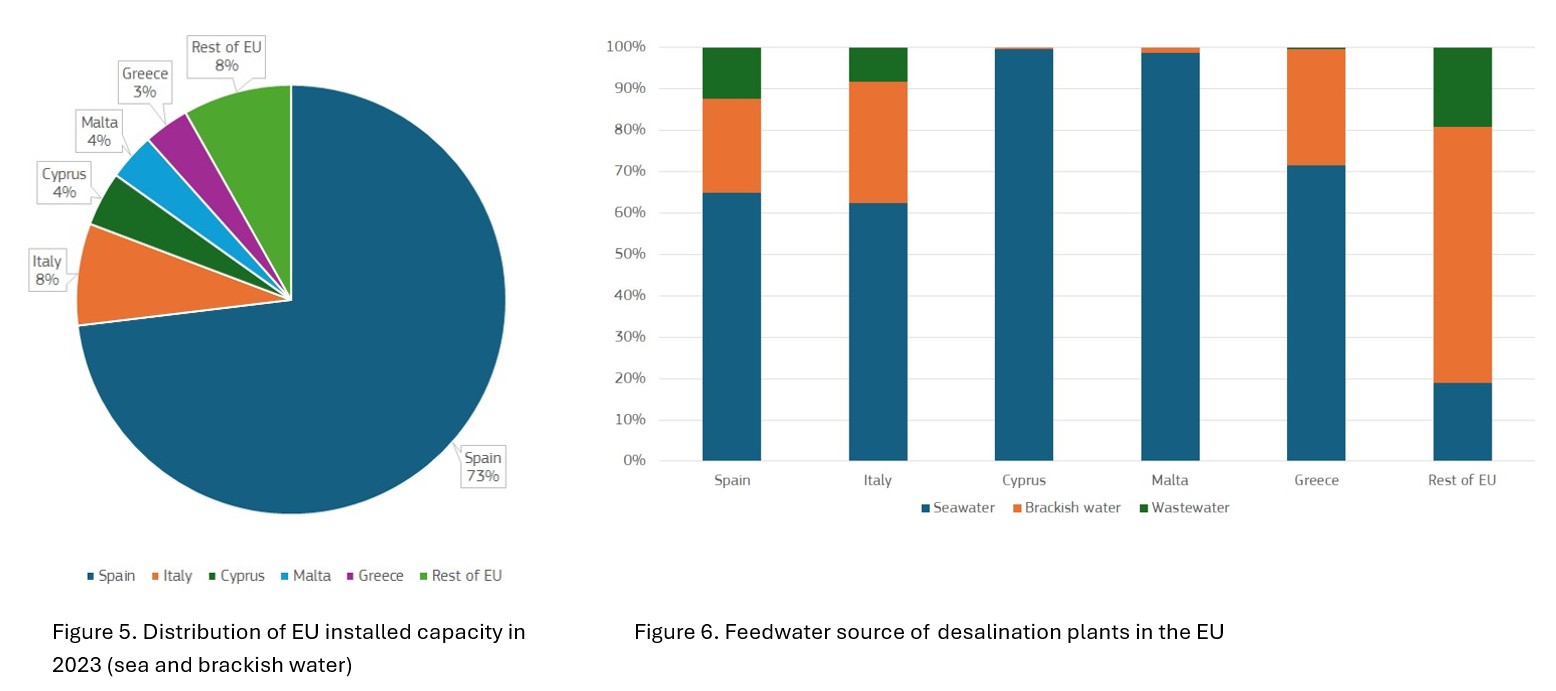

According to GWI’s DesalData, to date there are 1 901 active desalination facilities in the EU, which can supply 7.29 million m3/day of freshwater. These include facilities fed by seawater (43%), inland and/or brackish water (47%), as well as wastewater (10%)[16].

Active capacity has increased considerably over time. Desalination in the EU has developed almost exclusively in response to territorial water shortages in the early 1990s, with small plants supplying drinking water to hotels and resorts. Installed capacity has then grown significantly over the first decade of the century, with some large and extra-large plants commissioned to serve large coastal cities such as Barcelona and Alicante in Spain. Since 2010, most of the new capacity installed was in the form of small and medium size plants. From 5.08 million m3/day in 2009 to 7.29 million m3/day, active capacity has grown by more than 43% over the period (Figure 2).

The image shows a map that indicates the distribution of desalination plants in EU-27 in 2024

About 65% of the operational plants in the EU are located in coastal areas or offshore. The offshore plants support offshore activities, mostly oil and gas fields. The inland plants are used for the production of drinking water and industrial water; often through a process of purification of saline/brackish water present in local aquifers.

The geographical concentration of these plants is further illustrated in Figure 3.

Spain is by far the country with the largest desalination capacity in the EU, totalling nearly three quarters of total active capacity. It is followed by Italy, Cyprus, Malta and Greece (Figure 5).

In terms of uses, 68% of capacity is deployed for municipalities and tourist facilities as drinking water, 18% of industry uses and, 14% for irrigation, the rest consisting of demonstration and discharge facilities. Italy ranks first for industrial use with 28% of total capacity, shortly followed by Spain with 25% and the Netherlands with 10%.

In the Mediterranean Member States, most facilities use seawater as feedwater, whereas the situation reverses in the rest of the EU, with inland or brackish water used as the main source. Wastewater is a minor source of feedwater in the entire EU (Figure 6).

Climate change is imposing severe and escalating pressures on freshwater resources across Europe with significant implications for the agricultural sector, as rising temperatures, shifting rainfall patterns, glacier melting, and more frequent extreme weather events (droughts and floods) have already impacted crop yields, livestock production, and farmer livelihoods across the region[17]. Prolonged droughts have long been causing widespread agricultural losses affecting southern European countries most acutely but also causing impacts in central and northern areas previously unaffected by water scarcity[18]. Recent estimates put the current annual losses due to drought at around €9 billion for the EU and the UK, with the highest losses in Spain (€1.5 billion per year), Italy (€1.4 billion per year) and France (€1.2 billion per year), of which, depending on the region, those affecting agriculture range between 39-60%[19].

Projections indicate the agricultural impacts of climate change will intensify in the coming decades as, under medium and high emission scenarios, droughts that currently occur every 100 years could happen every 10-30 years on average in southern Europe by the 2070s[20]. Such intensification threatens severe, widespread consequences for European agriculture, potentially endangering regional food security[21]. Against this backdrop, desalination is considered as a promising option for making agriculture less dependent on rainfall and utilising water sources that are considered unusable without treatment[22], such as inland brackish water and wastewater.

In Europe, Spain is increasingly reliant on desalination as a key water source for agriculture, as well as Greece and Cyprus, to supplement irrigation water, primarily for the growth of fruits, vegetables, and grapes.

Spain, for instance, has one of the world’s most extensive seawater desalination capabilities, with major facilities, such as Torrevieja, Alicante I and Valdelentisco plants. These facilities employ reverse osmosis technology to produce over 200 million m3 of water annually. Besides being supplied to the municipalities as drinking water, this water is channeled to irrigation districts in the southeastern Murcia region, which predominantly produce fruit, vegetables, and grapes[23]. Studies suggest that, during drought periods, when surface water resources are strained, desalinated water constitutes between 50-80% of the total agricultural irrigation supply in this region.[24]

In Greece, a combination of seawater desalination and treated wastewater reuse fulfills up to 60% of the irrigation demand for major greenhouse horticulture crops, including tomatoes. This approach is particularly crucial in drought-prone areas around Athens during the summer months[25]. Similarly, on the Island of Cyprus, where seasonal droughts are a common occurrence, brackish water desalination and seawater desalination account for over 15% of the total agricultural irrigation supply.[26]

Here, citrus fruits are particularly reliant on desalinated water for growth. However, studies indicate risks associated with the long-term use of desalinated water for irrigation, including soil salinisation. This requires more effective regulation on appropriate irrigation methods and crop selection to prevent soil degradation[27]. For example, desalinated water requires boron control in order to avoid toxicity to plants, a cost-intensive process which can be mitigated if the water is blended with other sources.

Some of the main challenges and opportunities to scale up desalination for agriculture include:

- The high cost of desalinated water and its negative environmental impact, primarily caused by energy requirements and brine management, remain major challenges. The estimated cost of desalinated water for irrigation ranges from 0.50€ to 2€ per cubic metre[28]. For comparison, farmers are often charged between 0.05€ to 0.35€ per cubic metre for surface irrigation water, while unconventional sources such as reclaimed wastewater may cost between 0.15€ to 0.60€ per cubic meter[29]. However, it should be noted that currently many European countries undervalue water from conventional surface and groundwater sources, which makes desalination appear expensive in comparison[30]. The greater cost of desalinated water makes it difficult to be competitive without subsidies, except for crops with high profit margins.

- Energy-wise, transitioning to renewable electricity sources, such as solar and wind, that are becoming cost-competitive with fossil fuels could reduce costs[31]. However, intermittent power generation from renewables affects reliability of water supply, necessitating storage or flexible on-demand operation capability. Pressurised irrigation techniques such as subsurface drip irrigation are amenable to the on-off intermittent supply patterns from renewables-powered desalination systems[32].

- While technical and economic hurdles remain, RO desalination of saline water coupled with renewable energy has promising potential to provide alternative irrigation water sources. RO has emerged as the most widely used and suitable desalination technology due to its modularity, declining costs, and reliability compared to thermal distillation processes[33]. To employ desalinated water for direct uses on soil, it has to be blended with other water sources, to compensate for its lack of nutrients (calcium, magnesium, sulphur) needed for plant growth and soil health, and must undergo a targeted remineralisation to reduce its corrosivity[34].

- Desalination can help replenish the water cycle: when desalination is coupled with water reuse for irrigation, there is a net transfer of water to the land phase of the hydrologic cycle. This may help mitigate the hydrological impacts of climate change in regions such as southern Europe. In addition to reducing groundwater abstraction, reuse of desalinated water for irrigation can for example facilitate agriculture, ecosystem restoration and vegetation growth in otherwise unproductive regions[35].

As regards brine disposal, it can become an issue when considering the use of desalination plants to support agricultural water needs. There have been several studies on how to mitigate the negative effects of brine[36], but also on how to use it to agricultural advantage, such as reusing it in hydroponic culture[37].

The desalination market encompasses the following segments:

- Desalination research and development (i.e. activities related to the technological innovation, prototyping, testing, as well as designing and engineering of desalination processes and plants);

- Desalination project financing (i.e. activities of financial institutions and banks providing specialized financial services and intermediation, including the structuring of special purpose vehicles);

- Desalination equipment (i.e. manufacturing and construction of desalination plants, manufacturing of desalination components, supplies and equipment, preparation and building of desalination facilities, pipelines, energy recovery devices, etc.);

- Desalination services (i.e. segment that includes a broad range of civil, technical, mechanical, commercial, contractual, environmental, energy, regulatory compliance, and laboratory services required for the installation, integration, maintenance, upgrade and operation of desalination plants);

- Operation of desalination plants (i.e. activities related to the intake, pre-treatment and filtering of seawater, functioning of the desalination plant, waste management, distribution of desalinated water).

The economic size of the desalination market in the EU requires estimating complementary segments across the desalination value chain. In the absence of official disaggregated statistics on turnover, value added and employment for each of these segments at the EU level, the turnover of the desalination operation segment can be estimated by using average costs of producing desalinated water and installed capacity as reference indicators (Figure 7)[37].

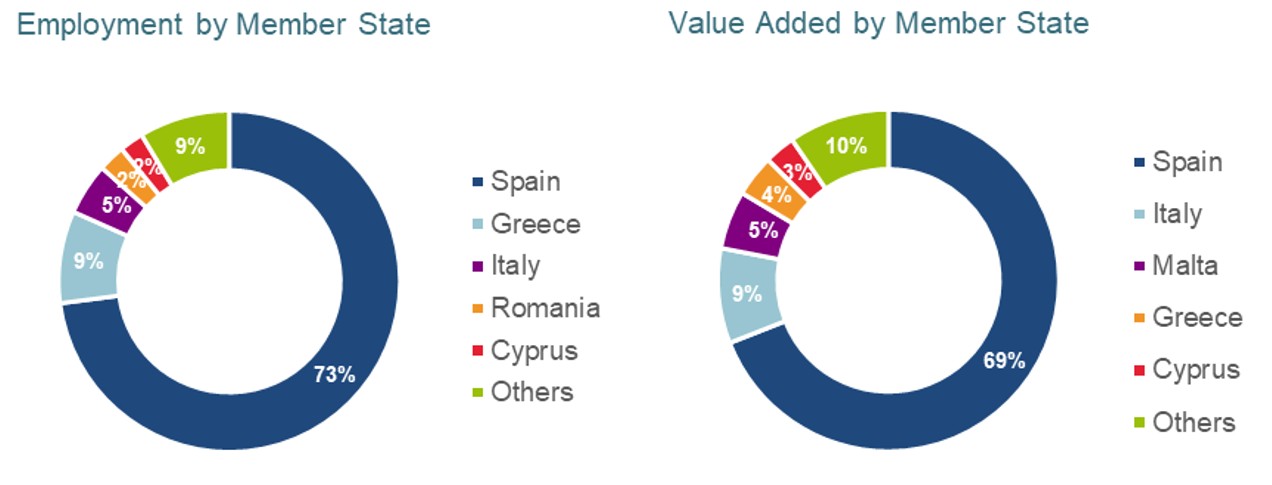

Spain largely dominates the desalination operation market, employing nearly 73% of the subsector’s workforce (5,596 persons) and generating 69% of its GVA (EUR 422 million) (Figure 8).

The development of desalination projects is characterised by intricate economic and financial considerations, primarily due to the substantial size and cost of these assets. Structuring such projects necessitates a comprehensive understanding of the typical value chain and the diverse participants involved. Additionally, the choice of development models significantly influences financing strategies and outcomes.

The desalination sector is a mature one, with a high level of standardization, with well-established frameworks for project structuring—particularly in regions like the GCC, where independent water and power projects (IWPPs) or independent water producers (IWP) follow consistent public-private partnership (PPP) models. Global benchmarks (e.g., from IRENA, World Bank, and SWCC) are routinely used to assess and compare projects.

All desalination projects undergo a phase of master planning aiming at identifying the size, siting of plant and infrastructural needs (e.g. for water transmission) followed by a feasibility phase and a preliminary environmental approval.

Afterwards, the development of desalination assets involves a complex value chain, typically encompassing three main phases:

- Bidding: the initial phase where project proposals are solicited and evaluated, on the basis of financing arrangements to be subscribed at the time of the contract award.

- Design and construction: this phase includes permitting and licensing, entitlement, technology selection, construction, regulation compliance, commissioning and performance testing.

- Operation: post-commissioning, this phase focuses on the facility's operation and maintenance, addressing aspects such as the quality of source water, power supply, and demand for desalinated water.

The desalination industry has become increasingly standardized, de-risked, and bankable over time, especially for large-scale RO projects. Each phase involves diverse players, reflecting the technical complexity of the facilities being developed. There is a general trend towards increased specialisation among these players. Project sponsors are increasingly seeking economies of scale through the development of larger assets, particularly in the case of reverse osmosis technology. The roles of actors and contractual interfaces are highly standardized in modern desalination projects, especially under IWPP frameworks where an IWP establishes a special purpose vehicle (SPV) company, where the client public corporation may or may not have equities, to develop the project and sell water. The SPV, in turn, may have the option to award a contract to an engineering, procurement and construction (EPC) operator. As an alternative, public corporations can directly award a turnkey contract to EPC operators.

Desalination risks (including permitting and licensing, technology selection, construction challenges, regulatory compliance, financial arrangements, source water quality, power supply reliability, and fluctuations in water demand) are increasingly well-understood, mitigated, and transferred along these contractual interfaces.

Fully integrated models including IWPPs / IWPs are now practically a standard. The development of desalination projects involves selecting appropriate procurement contracts between private entities and local governments or authorities. Given the high costs and long lifespans of desalination assets, these choices are crucial in effectively distributing responsibilities and risks. The (mostly private) developers take on end-to-end responsibilities, including financing, construction oversight, and long-term operation and maintenance.

Three main project delivery methods are commonly employed in the desalination sector, each varying in the degree of public and private involvement and associated risk allocation[38]:

- Build-Operate-Transfer (BOT) / Build-Own-Operate-Transfer (BOOT): in these models, private entities finance, construct, and operate the desalination facility for a specified period before transferring ownership to the public authority. This approach allows public authorities to leverage private capital and expertise while deferring ownership responsibilities until after the operational phase.

- Design-bid-build (DBB): Here, the public authority separately contracts the design and construction phases, maintaining significant control over the project. However, this method may result in fragmented responsibilities and potential inefficiencies due to the separation of design and construction contracts.

- Design-Build-Operate (DBO): under this model, a single private contractor is responsible for the design, construction, and operation of the facility. The public authority retains ownership and financing responsibilities, while the contractor assumes operational risks, potentially leading to more integrated and efficient project delivery.

The degree of risk assumed by private and public entities varies across different models. In BOOT arrangements, private operators assume most project risks, including financing, construction, and operation. They recover investments and operational costs over the project's lifespan through long-term agreements with public authorities. In DBO contracts, on the other hand, the public authority outsources design, construction, and operation phases to a contractor, who typically does not bear financing risks. The contractor is paid for design and construction upon completion and receives an operating fee during the operational period. The agreements are typically non-recourse finance deals.

Reverse-osmosis desalination facilities present challenges due to the sensitivity of membrane performance to feedwater quality variations. Long-term performance assessments during commissioning are difficult, as key operational variables, such as membrane and filter replacement rates, can only be verified well after commissioning. Consequently, DBO contracts may include an operational period of two to five years to address these uncertainties[39]. As membrane fouling risks can be mitigated by proper pretreatment, membrane suppliers may also provide a membrane replacement rate guarantee which allows the operator to replace membranes at no cost provided that pre-treated water quality is compliant with agreed conditions.

BOOT schemes have gained popularity in the desalination sector due to their ability to allocate significant financial risks to private partners. These arrangements often involve long-term Water Purchase Agreements (WPAs) between the private owner/operator and the local water authority. The WPAs specify conditions for water delivery, including quantity, quality, delivery pressure, and tariffs. Tariff structures typically encompass fixed capacity payments to cover capital costs and variable payments for operational expenses. The public authority retains in these cases only the risks related to the demand for water and the risk that seawater quality fall outside a certain design envelope.

Desalination is fast becoming a conventional method for water treatment globally. In line with global trends, the European desalination market is expected to enter an expansionary phase not only to address the consequences of climate change, but also to embrace policy-driven technological developments to reduce its operational costs and environmental impacts. Two main trends can be observed in the market. On the one hand, large-scale plants are becoming more common, with capacities growing due to advancements that lower unit costs. On the other hand, smaller scale desalination plants are gaining traction for municipal purposes, often combined with architecturally elegant structures, in order to increase resilience and decrease energy costs due to far distance transportation.

Numerous EU initiatives are encouraging investments in sustainable desalination technologies, among others. This includes BlueInvest, the EU initiative aimed at accelerating innovation and investment opportunities in the sustainable blue economy. To-date, the initiative has distributed grants for EUR 43.8 million, provided technical assistance to more than 70 companies, and supported blended finance instruments for blue economy start-ups and scale-ups[40]. Furthermore, the EU Sustainable Finance Taxonomy[41] classifies desalination projects as environmentally sustainable if they meet specific criteria. These criteria include using energy efficiently, keeping greenhouse gas emissions low, and minimising harm to biodiversity. In practice, this means new desalination plants should maximise the use of renewable energy and ensure that brine discharges are safely managed (diluted or treated) to avoid marine damage. Projects that fulfil such requirements can be eligible for green financing and possibly national or EU subsidies. For example, the EU’s Recovery and Resilience funds and other financing instruments have been used by Member States to support the development of climate-resilient water infrastructure, including desalination[42].

Over recent decades, improved membrane technologies (especially reverse osmosis) and energy recovery devices have driven down the cost of desalination significantly. Advanced research and economies of scale have helped reduce costs by as much as 60% over the past decade. Increased automation and smart monitoring systems also help optimise performance and reduce downtime. It has been noted that life-cycle desalinated water costs have fallen globally over the last 20 years from an average of USD 1.25-1.50 per m3 in the early to mid-1990s to less than USD 0.75 per m3 in 2012[43], and the trend has not reversed. This trend is mainly due to the adoption of RO instead of thermal technologies.

Given that energy costs can account for 40–60% of the overall desalinated water cost, there is a strong industry push to couple desalination plants with renewable energy sources (such as solar and wind)[44], especially in the case of small decentralised and off-grid plants. This integration not only reduces operating costs but also aligns desalination with global decarbonisation efforts. In the EU, projects such as PRODES (2005-2008), DESALIFE, DESOLINATION, and SOL2H20 are sheer examples of the increasing efforts in reducing the environmental footprint and costs of desalination by leveraging renewable energy.

Beyond conventional reverse osmosis, emerging technologies – such as membrane distillation, forward osmosis, and capacitive deionization – are under development. Although unlikely to reach large scale in the short run, these methods aim to further improve energy efficiency and reduce environmental impacts, particularly in brine management (Box 1).

Box 1. Brine: from a threat to the marine environment to an opportunity for the economy The concept of circular economy has at its core the goal to eliminate waste and promote the continual use of resources by designing products for longevity, reuse, repair, and recycling. Desalination is no exception. Brine is the “unwanted” by-product of desalination processes, a hot concentrate of dissolved salts and other minerals, whose disposal is an environmental concern due to the potential impacts on marine ecosystems. SEA4VALUE, a H2020-funded project, is designing and implementing technologies for recovering minerals and metals from seawater desalination brines. The aim is to make desalination plants the third source of valuable raw materials in the European Union. Not only does the project have the potential for securing the supply of critical raw materials such as magnesium, boron, scandium, gallium, vanadium, indium, and lithium, but it can also contribute to making desalination more economically efficient by valorising its by-products. |

While these technologies are primarily in the research and pilot-scale stages, they bear a significant potential:

- Membrane distillation is a thermally driven process where a hydrophobic membrane separates a heated saline solution from a cooler permeate side. The temperature difference induces water vapour to pass through the membrane, leaving salts and impurities behind. Advantages of membrane distillation include operation at lower temperatures and pressures compared to conventional thermal processes, making it suitable for integrating with low-grade or waste heat sources. However, challenges such as membrane fouling and scaling, along with relatively low flux rates, have limited its widespread adoption[45].

- Forward osmosis utilises the natural osmotic pressure difference between a saline feed solution and a concentrated draw solution to induce water flow through a semipermeable membrane. This process requires less hydraulic pressure than reverse osmosis, potentially reducing energy consumption. Forword osmosis is advantageous in treating high-salinity or contaminated waters and can be coupled with other processes for draw solution recovery. Nevertheless, issues like membrane fouling, draw solution regeneration, and lower water flux present ongoing challenges[46].

- Capacitive deionization is an electrochemical technique where ions are removed from water by applying an electrical potential across porous electrodes, causing ions to adsorb onto the electrode surfaces. This method is energy-efficient, especially for low to moderate salinity waters, and operates at ambient pressure without the need for high-pressure pumps. However, its effectiveness decreases with increasing feed water salinity, and electrode material degradation over time remains a concern[47].

- Nanofiltration is a pressure-driven membrane separation process that filters water through membranes with pore sizes typically less than 2 nanometres. Positioned between ultrafiltration and reverse osmosis in terms of selectivity, nanofiltration effectively removes divalent ions and larger molecules while allowing most monovalent ions to pass through. It operates at lower pressures than reverse osmosis, leading to reduced energy consumption. Studies have shown that nanofiltration can be as effective as reverse osmosis in desalination while consuming approximately 29% less energy[48].

The ultimate goals of new technologies are to reduce energy consumption and/or increase the recovery rate, that is the proportion of intake water that is converted into high quality (low salinity) water for sectoral use.

8The term diluate specifically refers to the solution that has been desalinated in electrodialysis processes, where dissolved ions are removed by an applied electric potential across ion-exchange membranes. This term is frequently used in technical and engineering literature on membrane processes, as highlighted in the work of Elimelech & Phillip (2011) in The future of seawater desalination: Energy, technology, and the environment (Science, 333(6043), 712-717), and Strathmann (2010) in Electrodialysis, a mature technology with a multitude of new applications (Desalination, 264(3), 268-288).

9 Bisselink B., Bernhard J., Gelati E., Adamovic M., Guenther S., Mentaschi L., Feyen L., and de Roo, A, Climate change and Europe’s water resources, EUR 29951 EN, Publications Office of the European Union, Luxembourg, 2020, ISBN 978-92-76-10398-1, doi:10.2760/15553, JRC118586.

10 Of these, 11,724 are currently operating, representing 85% of the total number of facilities and accounting for 92% of the global capacity.

11 Jones, E., Qadir, M., van Vliet, M. T., Smakhtin, V., & Kang, S. M. (2019). The state of desalination and brine production: A global outlook. Science of the Total Environment, 657, 1343-1356

12 Eyl-Mazzega M.A. and É. Cassignol, (2022). The Geopolitics of Seawater Desalination, Études de l’Ifri, IFPRI, September 2022.

Sirota, R., Winters, G., Levy, O., Marques, J., Paytan, A., Silverman, J., ... & Bar-Zeev, E. (2023). Impacts of Desalination Brine Discharge on Benthic Ecosystems. Environmental Science & Technology.

19 Cammalleri C., Naumann G., Mentaschi L., Formetta G., Forzieri G., Gosling S., Bisselink B., De Roo A., and Feyen L, JRC Technical Report, 2020, “Global warming and drought impacts in the EU”, doi: 10.2760/597045

23 Del Amor et al. 2020. Integrated Water Management in Southeast Spain: Assessment of Total Water Cycle. Water. 12(6):1803.

24 Martínez-Alvarez et al. 2016. Seawater Desalination for Crop Irrigation – A Review of Current Experiences and Revealed Key Issues. Desalination. 381: 58-70.

25 Chartzoulakis et al. 2010. Water Resources Management in Crete (Greece) including Water Recycling and Desalination. Agricultural Water Management. 98(1): 96-105

26 Polycarpou and Zachariadis 2013. An Econometric Analysis of the Use of Desalinated Water in Cyprus. Water Resources Management. 27(7): 2089-2101.

27 Poulakis et al. 2015. Overview of Water Quality Problems in Three Regions of Intensive Agriculture in Greece and Agricultural Practices to Minimize the Impact on Water Resources. Global Nest Journal. 17(4): 721-732.

37 Based on data released by AEDyr, the Spanish desalination association (https://aedyr.com/en/) and DesalData, respectively.

38 Technology, Committee & Board, Water & Studies, Division & Council, National. (2008). Desalination: A national perspective. 10.17226/12184.

39 Voutchkov, N. (2019). The Role of Desalination in an Increasingly Water-Scarce World.