The Marine living resources sector encompasses the harvesting of renewable biological resources (primary sector), their conversion into food, feed, bio‐based products and bioenergy (processing) and their distribution along the supply chain.

The Marine living resources sector comprises three sub-sectors:

primary sector: capture fisheries (small-scale coastal, large-scale and industrial fleets) and aquaculture (marine, freshwater and shellfish);

processing of fish products: processing and preservation of fish, crustaceans and molluscs; meal preparation, manufacture of oils and fats and other food products;

distribution of fish products: retail sale of fish, crustaceans and molluscs in specialised stores and wholesale outlets.

The exploitation of marine biological resources is analysed in this section, as well as in Blue biotechnology.

The EU is the eighth largest producer of fishery and aquaculture products (behind China, Indonesia, India, Vietnam, Peru, the Russian Federation and the United States of America), covering around 2% of global production1. Overall EU production has been rather stable in the last few decades. The EU has slightly more than 54,200 active vessels landing about 3.6 million tonnes of seafood worth €6 billion in 20212; while the EU aquaculture production represented about 25% of the total EU seafood production with about 1.2 million tonnes worth €4.3 billion.

The EU marine living resources sector has been heavily impacted by external factors in recent years. The Trade and Cooperation Agreement (TCA) following BREXIT gradually reduces the share of EU fishing opportunities in UK waters stocks from 2021 to 2025. The Covid-19 pandemic and public health interventions depressed demand and disrupted supply chains for many fishing businesses in 20203. The military invasion of Ukraine by Russia in February 2022 resulted in an increase in energy and fuel prices, as well as in general inflation, until the end of 20224. Fuel prices went consistently below €1 per litre only after November 2022, allowing the primary sector to recover its economic performance from 2023. The impacts on the processing and distribution sectors have been milder as they have relied on imports to fill the gap in domestic production.

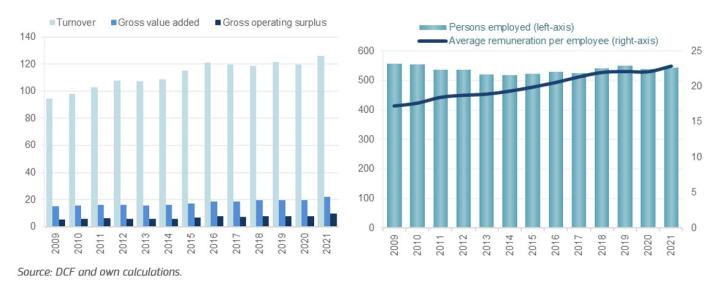

The sector generated more than €22.0 billion in GVA in 2021, a 13%-increase compared to 2020. While gross profits increased by 24%, reaching €9.7 billion, the reported turnover was about €126 billion.

The sector directly employed more than 543 000 persons, a 1%-increase from 2020. The annual average wage is estimated at €22.800, a 4%-increase from 2020 (Figure 1).

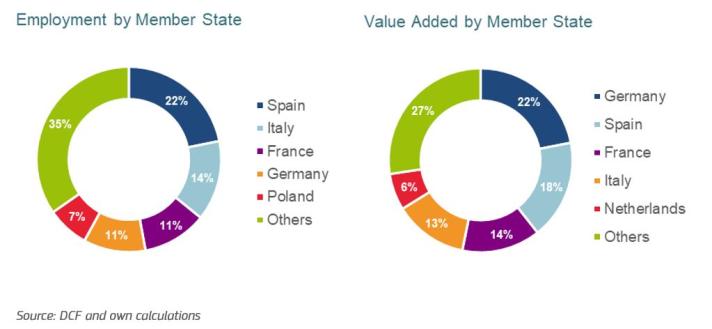

Spain leads the sector in employment with 22% of the jobs, followed by Italy with 14%, and France and Germany with 11% each. Germany generates 22% of the GVA, followed by Spain with 18%, France with 14% and Italy with 13% (Figure 2).

Employment: Distribution of fish products employed about 211 300 persons, accounting for 39% of jobs, while Primary production employed slightly more than 200 200 persons (37%) and Processing of fish products about 131 500 persons (24%).

Gross value added: In 2021, the distribution of fish products generated €11.7 billion GVA, about 53% of the sector, followed by Processing of fish products with €5.8 billion (26%) and Primary production with €4.5 billion (20%).

Overall economic indicators in 2021 displayed an improvement compared to 2020, reaching the historical maximum. Estimates suggest that the performance of the sector will be slightly worse in 2022, due to the increase in fuel prices and inflation.

The economic performance of wild-capture fisheries and aquaculture is in line with the one in 2020 and worse than in 2019. However, for the fish processing and especially distribution, performance reached its maximum in 2021, partly thanks to the increasing imports of seafood products.

In 2022, household expenditure on fishery and aquaculture products in the EU reached EUR 62.9 billion, marking an 11%-increase from 2021. The average consumption per capita is estimated at 23.71 kg (measured in live weight equivalents) of fishery and aquaculture products in 2021, which represented a 2% increase from 20205. Most EU consumption of fishery and aquaculture products consists of wild products (about 70%) and, more specifically, of imported fishery products.

The EU’s self-sufficiency is estimated to have reached its lowest level with 38.2% in 20216. Self-sufficiency is the capacity of EU Member States to meet their citizen’s demand for seafood from their own production. Hence, the EU is able to maintain its consumption of fishery and aquaculture products by importing them from other regions of the world.

In the EU, the fish processing industry strongly relies on imports from third countries: salmon and cod from Norway and the UK, Alaska pollock from China, shrimp from South and Central America and South-East Asia, sardines from Morocco, squid, tropical tuna, etc.

In 2022, a substantial growth in the value of extra-EU imports was reported. It could not be solely attributed to the consequences of the Covid-19 pandemic recovery, which led to sudden spikes in demand and increases in prices; it was also a consequence of lower domestic supply contributing to an increase in prices, which was due to the effect of lower quotas for a number of species and tightened competition on raw materials. Moreover, the Russian military invasion of Ukraine heavily contributed to the rise in value, affecting energy costs, and in turn production costs. In fact, it has been estimated that every 10 cents increase in the fuel price per litre would lead to a profitability loss of around €185 million in the EU fishing fleet7.

The Russian aggression also had a significant impact on exchange rates, which played a role in the increase in prices and overall values, affecting trade between countries on a global scale. In 2023, however, inflation was lower, whereas the imports kept on tightening, resulting in more stable prices and values.

High energy prices have affected the sector. Prices of raw materials such as soy, fishmeal and oil have also been impacted by the conflict, driving up overall prices in Marine living resources’ related industries, such as aquaculture8.

In 2023, the Commission presented a fisheries and oceans package9 which includes four initiatives. The main objectives of the measures are to promote the use of cleaner energy sources and reduce dependency on fossil fuels, as well as reduce the sector’s impact on marine ecosystems. This package includes the Communication on the Energy Transition of the EU Fisheries and Aquaculture sector (See Section on energy transition) with measures to improve its sustainability and resilience.

In the framework of the Communication on the Energy Transition, the Commission has released a dashboard on the EU Blue Economy Observatory, aimed at measuring the incremental impact of fuel prices on the economic performance of the EU fishing sector. Another key action in this area was the set-up of the Energy Transition Partnership, which was launched in 2023 and supported by a number of thematic workshops. These workshops will feed into the development of a common roadmap for the energy transition in EU fisheries and aquaculture.

Another important policy development has been the entry into force of the new EU Fisheries Control Regulation10. This revised EU fisheries control regulation updates most of the rules for fishing vessels to modern technology and promotes sustainability. The key changes involve enhanced monitoring of fishing activities, better traceability of catches and harmonised sanctions for rule violations. These revised rules modernise the way fishing activities are controlled for EU vessels and for non-EU vessels fishing in EU waters. They aim to prevent overfishing, create a more efficient and unified fisheries control system, and promote fairness among different sea basins and fleets.

In 2021, the EU fishing fleet numbered 54 213 active vessels, offering direct employment to almost 122 thousand persons, with an average annual remuneration of slightly more than €26 000. The EU fleet consumed 1.81 billion litres of fuel to land 3.56 million tonnes of seafood with a reported value of EUR 6 billion. The Gross Value Added (GVA) and gross profit (all excl. subsidies and fishing rights) were estimated at €3.3 billion and €1.19 billion, respectively11.

Figure 1: Size of the EU Marine living resources sector, 2009-2021. Turnover, GVA and gross operating surplus in € billion, persons employed (thousand), and average wage (€ thousand)

The two bar charts provide insights into the EU's Marine Living Resources sector from 2009 to 2021, focusing on key economic indicators.

First Bar Chart: Size of the EU Marine Living Resources Sector (2009-2021)

Turnover: This represents the total revenue generated by the sector annually. Over the period, the sector experienced fluctuations, with a notable increase in turnover by 2021, indicating growth in economic activities related to marine living resources.

Gross Value Added (GVA): GVA measures the sector's contribution to the economy by assessing the value of goods and services produced. The chart shows a general upward trend in GVA, reflecting the sector's increasing economic significance.

Gross Operating Surplus: This metric indicates the surplus generated after accounting for operating expenses, serving as an approximate measure of profitability. The data suggests a positive trend, with the surplus growing over the years, highlighting improved financial health within the sector.

Second Bar Chart: Detailed Economic Indicators (2021)

Turnover: In 2021, the sector reported a turnover of approximately €126 billion, marking a 13% increase compared to 2020.

Gross Value Added (GVA): The GVA for 2021 was about €22.9 billion, indicating the sector's substantial contribution to the EU economy.

Gross Operating Surplus: The sector achieved a gross operating surplus of €9.7 billion in 2021, reflecting a 24% increase from the previous year, suggesting enhanced profitability.

Employment: The sector directly employed over 543,000 individuals in 2021, representing a 1% increase from 2020, indicating stability and slight growth in job opportunities.

Average Wage: The annual average wage in the sector was estimated at €22,800 in 2021, showing a 4% increase compared to 2020, reflecting improvements in employee compensation.

These charts collectively depict a sector that has experienced growth in revenue, economic value, profitability, employment, and wages over the specified period, underscoring its vital role in the EU's blue economy.

Figure 2: Share of employment (left) and GVA in EU Maritime living resources sector (right) in 2021

The chart presents the distribution of employment and Gross Value Added (GVA) in the EU's Maritime Living Resources sector for 2021, broken down by Member State. Here's a detailed breakdown:

Employment Share by Member State (Left Side of the Chart):

Spain: Leading the sector with 22% of total employment, Spain's workforce in this sector is approximately 119,460 individuals.

Italy: Accounting for 14% of employment, Italy has around 76,020 individuals employed in the sector.

France: Contributing 11% to the sector's employment, France employs about 59,730 individuals.

Germany: Also at 11%, Germany's employment in this sector is approximately 59,730 individuals.

Other EU Member States: The remaining 42% of employment is distributed among other EU countries, totalling around 228,060 individuals.

GVA Share by Member State (Right Side of the Chart):

Germany: Leading in GVA contribution with 22%, Germany's share amounts to approximately €4.84 billion.

Spain: Contributing 18% to the sector's GVA, Spain's share is about €3.96 billion.

France: At 14%, France's GVA contribution is approximately €3.08 billion.

Italy: Accounting for 13% of the GVA, Italy contributes around €2.86 billion.

Other EU Member States: The remaining 33% of GVA, totalling about €7.26 billion, is generated by other EU countries.

This distribution highlights that while Spain leads in employment within the Maritime Living Resources sector, Germany surpasses in economic contribution as measured by GVA. The data reflects the varying scales and efficiencies of maritime activities across different EU Member States.

1 EUMOFA. 2023. The EU fish market, 2023 edition. Luxembourg: Publications Office of the European Union. doi: 10.2771/38507.

2 STECF. 2023. The 2023 Annual Economic Report on the EU Fishing Fleet. Publications Office of the European Union, Luxembourg.

3 Carpenter, G., Carvalho, N., Guillen, J., Prellezo, R., Villasante, S., Andersen, J. L., ... & Zhelev, K. (2023). The economic performance of the EU fishing fleet during the COVID-19 pandemic. Aquatic Living Resources, 36(2).

4 Guillen, J., Carvalho, N., Carpenter, G., Borriello, A., & Calvo Santos, A. (2023). Economic Impact of High Fuel Prices on the EU Fishing Fleet. Sustainability, 15(18), 13660.

5 EUMOFA. 2023. The EU fish market, 2023 edition. Luxembourg: Publications Office of the European Union. doi: 10.2771/38507.

6 EUMOFA. 2023. The EU fish market, 2023 edition. Luxembourg: Publications Office of the European Union. doi: 10.2771/38507.

7 Guillen, J., Carvalho, N., Carpenter, G., Borriello, A., & Calvo Santos, A. (2023). Economic Impact of High Fuel Prices on the EU Fishing Fleet. Sustainability, 15(18), 13660.

8 STECF. 2023. Economic Report on the EU aquaculture (STECF-22-17). Publications Office of the European Union, Luxembourg, doi:10.2760/51391.

9 Fisheries, aquaculture and marine ecosystems: transition to clean energy and ecosystem protection for more sustainability and resilience. Available at: https://ec.europa.eu/commission/presscorner/detail/en/IP_23_828.

10 Regulation (EU) 2023/2842 of the European Parliament and of the Council of 22 November 2023 amending Council Regulation (EC) No 1224/2009, and amending Council Regulations (EC) No 1967/2006 and (EC) No 1005/2008 and Regulations (EU) 2016/1139, (EU) 2017/2403 and (EU) 2019/473 of the European Parliament and of the Council as regards fisheries control.

11 STECF (2023). The 2023 Annual Economic Report on the EU Fishing Fleet. Publications Office of the European Union, Luxembourg.