The sector of Maritime transport includes the following sub-sectors:

- Passenger transport: sea and coastal passenger water transport and inland passenger water transport;

- Freight transport: sea and coastal freight water transport and inland freight water transport;

- Services for transport: renting and leasing of water transport equipment.

Globally, approximately 12 billion tons of traded goods were transported by sea in 2022, accounting for roughly 49% of total trade, nearly double the proportion transported by air (26%)1. Port calls from liquid bulk carriers (e.g. oil) forerun container ships and dry bulk carriers (e.g. grain).

Asia represents the biggest player of this sector, with 4.6 and 7 billion tonnes of goods loaded and discharged respectively. Europe follows with 1.6 and 1.7 billion tonnes2. Europe saw its average Liner Shipping Connectivity Index (LSCI), which measures the economic connectivity of the sector, drop in 2022, only recording a recovery in the second quarter of 2023. The most-connected European economies, as measured by the Liner Shipping Connectivity Index (LSCI), were Spain, the Netherlands and Belgium3, whilst the most connected EU ports were Rotterdam (NL), Antwerp (BE) and Hamburg (DE)4.

Short sea shipping (SSS) is defined as the maritime transport of goods between ports in the EU (sometimes including candidate countries and EFTA countries) on the one hand, and ports in geographical Europe, on the Mediterranean and Black Seas on the other hand. In 2021, it comprised 60.9 % of the total sea transport of goods to and from the main EU ports (almost 1.8 billion tonnes). Italy, the Netherlands and Spain accounted for almost 41% of EU short sea shipping in 2021. Liquid bulk (40%) was the dominant type of cargo in EU SSS, followed by dry bulk (21%), containers (17%) and Ro-Ro (15%)5.

In 2022, 348.6 million passengers were recorded in EU ports, a 16.7% decrease compared to pre-Covid (2019)6. Greece (20%), Italy (15%) and Denmark (12%) accounted for almost half the total number of passengers embarked and disembarked in EU ports. There is a minimal variance between the count of passengers disembarking ('inwards') and embarking ('outwards') at EU ports. This phenomenon underscores the predominant reliance on national or intra-EU ferry services for seaborne passenger transport in Europe.

Although the sector is recovering from the tough halt due to COVID-19, EU ports recorded 32% fewer cruise passengers passing through (roughly 10 million) than in 2019. Almost three quarters of these passengers passed through Italian, Spanish, and German ports in 20227.

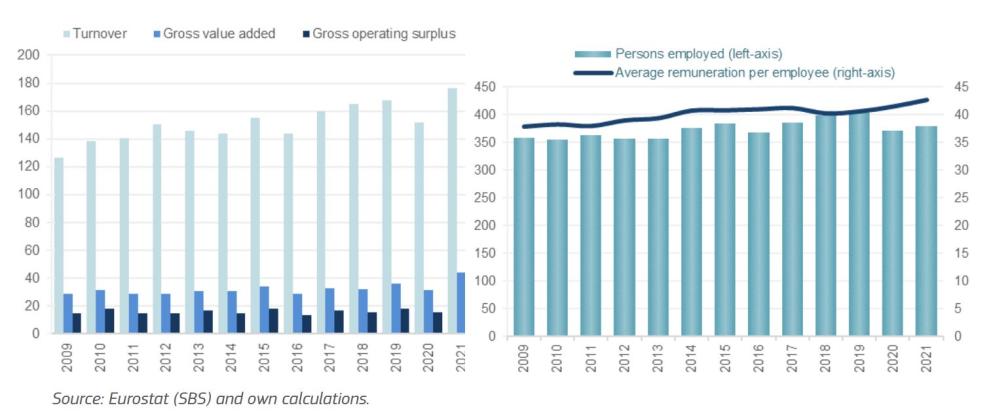

The sector generated a GVA of €44.3 billion in 2021, a 42% increase compared to 2020 and a 23% increase compared to the 2019 peak. At €28.1 billion, gross profit increased by 77% on the previous year. The turnover reported for 2021 was €176.7 billion, a 16% increase on the previous year.

In 2021, almost 380 000 persons were directly employed in the sector, 2% more than in 2020. The annual average wage was estimated at €43 000, up 3% compared to 2020.

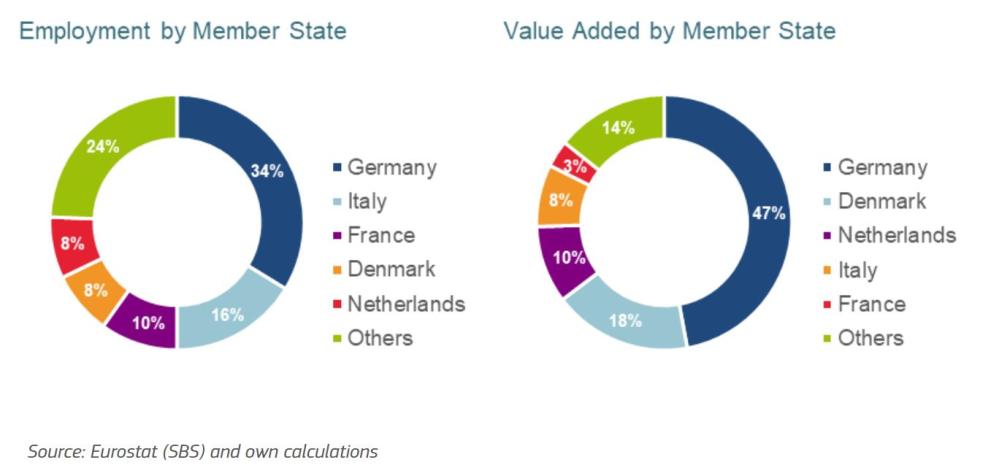

Germany leads employment within Maritime transport, contributing with 34% of the jobs, followed by Italy (16%) and France (10%). In terms of GVA, Germany generates 47% of the Members States’ GVA, followed by Denmark (18%) and the Netherlands (10%).

In 2021, about 50% of the jobs (190 000) were within the sub-sector Services for transport, while Passenger transport (95 000) and Freight transport both employed around 25% of people (94 000).

In terms of GVA, Freight transport generated about 58% of the sector’s GVA (€25.5 billion), followed by Services at 33% (€14.8 billion) and then Passenger transport at 9% (€4 billion).

For more detailed economic and social data, please consult the dashboard on the Blue Economy Indicators.

There are some factors that have influenced the maritime transport sector in the past years and others that are expected to significantly impact it in the near future. First, the Covid-19 pandemic had major consequences for economies, including the Maritime transport sector. The sector is involved in a major energy transition phase, directed by more stringent regulations in terms of emissions and industrial plans to facilitate the shift. Other factors are geopolitical (e.g., wars, disruptions in key maritime routes), technological (e.g., digitalisation), and financial (e.g., insurance).

The COVID-19 pandemic has affected the maritime transport sector. While the impact on cargo tonnage was relatively limited, the effects of COVID-19 on logistics and costs were profound. Container shipping prices rose to $11 108 in September 2021 from $1 389 in December 2019, and port congestion resulted in average port waiting days from 3.12 days to 9.78 days in developed economies due to higher demand for goods and limitations in port operations. This situation persisted until mid-2022, eventually stabilising and returning to pre-pandemic levels in 2023.

During the second quarter of 2023, SSS tonnage to and from major EU ports experienced a substantial decrease of 8.2% compared to the same quarter of 2022, totalling 505 million tonnes. Similarly, deep sea shipping tonnage also decreased by 6.4%, reaching 278 million tonnes. Looking at the overall annual variation, short sea shipping experienced a decrease of 8.7%, while deep sea shipping increased by 1.0% compared to the previous period. This increase in deep sea shipping can be attributed to the unprecedented distances travelled by oil cargoes in 2023, driven by the disruptions resulting from the Russian invasion of Ukraine. Oil and oil products began to travel longer distances as the Russian Federation sought new export markets and Europe found alternative energy suppliers. It is important to note that the presented values may vary depending on the reported transportation level, especially in relation to unknown associated regions. This reporting level was particularly high in the last three quarters of 2022 and the first two quarters of 2023.

Between Q2 2022 and Q2 2023, extra community international transportation decreased by 11.8% and intracommunity international transportation by 4.7%. Meanwhile, domestic transportation increased by 9.0%. The overall annual variation shows a 7.1% decrease in extra community international transportation, a 5.6% decrease in domestic transportation, and a 1.7% decrease in intracommunity international transportation.

The drop in extra community international transportation during the second quarter of 2023, compared to the same period in 2022, was primarily influenced by reduced maritime transportation with Europe, excluding the EU and Africa. While transportation in the Americas, Asia, and Oceania declined, the decrease was less pronounced. Looking at the overall annual change, maritime transportation in the Americas, Asia, and Oceania grew compared to the previous period. Conversely, there was a significant decrease in transportation in Europe, excluding the EU and Africa.

In terms of total gross weight of goods, the US continued to be the primary maritime transportation partner of the EU in the second quarter of 2023, maintaining this position for five consecutive quarters. The UK ranked as the second-largest maritime transportation partner of the EU during that period, followed by Norway, China, Turkey, Brazil, and Egypt. Russia experienced a continuous decline in its position, falling to the eighth place. Transportation between the EU, the US, and the UK represents nearly a quarter (24%) of the total maritime transportation outside the EU.

In response to the unprovoked Russian invasion of Ukraine, the UK, the US, and the EU have implemented a series of restrictive economic measures targeting the trade of Russian crude oil, refined petroleum products, and gas. These measures include import bans, pipeline transport restrictions, and a cap on the price of crude oil barrels, which notably affects underwriting processes for insurance. Consequently, there has been a significant shift in the trading patterns of these commodities. Additionally, the conflict has prompted European countries to seek alternative sources of energy, leading to increased imports of crude oil from Libya, Iraq, Norway, and Egypt, as well as liquefied gas and crude oil from the US East Coast, to compensate for the disruption of supplies from the Russian Federation.

The unprovoked invasion of Ukraine has served as a catalyst for change, forcing the EU to reassess and adjust its sources of energy imports. The decrease in dependence on oil and coal products from Russia, accompanied by an increase in imports from a variety of countries, reflects not only a reconfiguration of trade routes but also a strategic realignment with partners who share similar values. This adjustment is representative of a broader effort by Western economies to diversify their sources of supply and minimise geopolitical vulnerabilities. In parallel, there is a deliberate effort to reduce the EU's dependence on China in critical sectors such as technology and energy transition. Legislative initiatives such as the Inflation Reduction Act in the US, which promotes self-sufficiency in the manufacturing of critical components and encourages trade cooperation with select partners, are mirrored by similar strategies contemplated or already implemented within the EU. These measures not only have the potential to alter established maritime trade routes but also to redefine global economic alliances. Additionally, trade conflicts and tensions among major economies, such as the US and China, along with events like Brexit in the UK, have added complexity to global supply chains, affecting decisions on commercial routes and strategic alliances8.

Disruptions in key maritime routes like the Suez and Panama Canals due to crises and environmental challenges have led to increased freight costs and insurance premiums, prompting the search for alternative routes that may escalate fuel consumption and CO2 emissions. In this context, maritime security has gained prominence, particularly in strategic areas like the Red Sea and the Black Sea, where conflicts have reshaped global oil and cereal trade9.

The reconfiguration of global supply chains is another critical aspect of this new trade landscape. The search for efficiencies, new markets and diversification of production to reduce the risks of disruption are responses to an increasingly complex operating environment. Adaptability and resilience have become guiding principles, forcing companies and supply chain managers to rethink their previous strategies and practices. In addition, the response to the grain supply disruption caused by the unprovoked invasions of Ukraine, through initiatives such as the Black Sea, exemplifies how diplomacy and international agreements can mitigate the effects of geopolitical crises on maritime trade. These efforts seek not only to secure the flow of essential goods but also to stabilise global markets in times of uncertainty.

Maritime transport, central to international trade, faces significant challenges on its path to digitalisation. Despite its importance, only a small percentage of cross-border transactions in the EU are executed fully digitally, without the need for physical documents at any stage of the process. In comparison, aviation shows a higher adoption of electronic information exchange, at around 40%, while rail reaches just around 5%. Digitalisation in shipping is considerably lower, practically non-existent (1%).

This situation can be attributed in part to legal and technical barriers. For example, the need for handwritten signatures on transport documents in some countries represents a considerable obstacle to implementing digital solutions. The absence of uniform standards and a consolidated digital infrastructure also complicates interoperability between the different systems used in the sector.

Faced with these challenges, the EC has promoted initiatives such as the Digital Transport and Logistics Forum (DTLF), seeking to bridge the digital divide in this area. The introduction of Regulation (EU) 2020/1056 on electronic freight transport information (eFTI) marks a step forward, establishing a legal framework that facilitates the exchange of information electronically in maritime transport, which represents a crucial advance towards the modernisation and efficiency of the sector.

Maritime Autonomous Surface Ships (MASS)

A major digitalisation trend is the coming of the Maritime Autonomous Surface Ships (MASS). These vessels, depending on their degree of automation, can range from steering and navigational assistance to full automation of navigation. While there are not currently ships in the third degree, conditional automation (being full automation in the 5th degree), this trend is seen as a way to reduce operational costs, improve working conditions, save fuel by optimising routes, and reduce human errors and accidents. The European Maritime Safety Agency (EMSA) is providing support through the SafeMASS project by identifying risks and regulatory gaps, and Horizon 2020 projects are also tackling the topic, like the Autoship project (building and operating two autonomous inland vessels), the AEGIS project (autonomous navigation and cargo handling), and MOSES project (autonomous vessel manoeuvring and docking scheme)10.

S-100 Universal Hydrographic Data Standard

In 2019, the International Hydrographic Organization (IHO) released the S-100 Universal Hydrographic Data Model. This standardised framework, which substitutes the previous S-57, supports the development of interoperable marine data, including navigational charts, bathymetric data, seabed features, and other relevant information used for maritime navigation, safety, and management. This will allow systems to better exchange hydrographic and navigational data, enhancing navigation, research, and all other maritime activities. While the finalised edition was released in 2021, work on development and implementation has been ongoing, and operational data is expected to start a progressive release around 2024.

Insurance is a key activity for all maritime sectors, as every vessel, seafarer, and liability has, generally, some form of insurance. Maritime transport is particularly impacted by it because of the relevance of cargo insurance. More than half of maritime insurance premiums are in the category of Transport/Cargo. The seaborne transport leadership of (continental) Europe can also be appreciated for its leadership in maritime insurance premiums and their rising trend since 2019.

The market for cargo insurance was, in broad in economic terms, not affected by the COVID-19 epidemic – which is coherent with cargo transport data–, the logistical issues (e.g. port congestion) have been resolved, and, for Europe, are rising in a post-pandemic economic recovery trend. The sector is nevertheless challenged by the increase in extreme weather conditions, fires on-board vessels, increasing value and risk accumulation on single vessels/ports, and increasing geopolitical tensions11.

The European climate law makes reaching the EU’s climate goal of reducing EU emissions by at least 55% by 2030 a legal obligation. While maritime transport is one of the most efficient means of transport, it is estimated to cause 13.5% of EU transport emissions . Globally, it is responsible for roughly 3% of emissions caused by human activities.

The ‘Fit for 55’ package includes reforms to the maritime transport sector. Among these reforms, the EU emissions trading system (EU ETS) has been introduced in 2024 and will limit the emissions of large ships (above 5 000 GT) carrying goods and passengers departing from and arriving in EU ports, regardless of their flag12. The system covers 50% of emissions from voyages starting or ending outside of the EU, and 100% for voyages occurring between two EU ports and when ships are within EU ports. The reform initially covers CO2 emissions only, with methane and nitrous oxide scheduled from 2026 onwards. The system builds on the provisions in place for other EU ETS sectors as well as the revised EU Monitoring, Reporting and Verification regulation for maritime transport, according to which vessels are obliged to report the amounts of CO2 emitted. Generated revenues will be channelled into the Innovation Fund to drive innovation of the sector and accelerate the decarbonisation process.

Still in the context of the ‘Fit for 55’ package, the EC proposed the Alternative Fuels Infrastructure Regulation13. Specifically on the maritime sector, the regulation sets targets for the deployment of shore-side electricity supply for certain seagoing container and passenger ships (above 5 000 GT) in maritime ports. Ports that have an average annual number of calls over the last three years of 50, 40 and 25 for containerships, seagoing ro-ro passenger ships and high-speed passenger crafts, and other passenger ships respectively, must guarantee sufficient shore-side power output to meet at least 90% of that demand.

Furthermore, the FuelEU maritime regulation will oblige vessels above 5 000 GT calling European ports, with exceptions such as fishing ships, to reduce GHG intensity of the energy used on board gradually. By 2025, these vessels will be required to reduce the annual average carbon intensity (compared to a 2020 baseline) by 2%, to as much as to 80% by 2050. Also, the vessels will be obliged to connect to onshore power supply for their electrical power needs, unless they use another zero-emission technology.

Decarbonising the maritime industry will require a shift in technology (fuel cells, internal combustion engines) and operations to increase energy efficiency (slow steaming, cleaning and coating, waste heat recovery, hull and propeller design) as well as an uptake of alternative fuels (nuclear, hydrogen, ammonia, methanol) and renewable energy sources (wind, solar)14. These all have implications for the shipbuilding sector for both in terms of new builds and retrofitting technology in existing vessels.

The Net-Zero Industry Act (NZIA), as part of the Green Deal Industrial Plan, could enhance the competitiveness of the EU shipping sector by directing essential investments toward clean technologies and production capacity of shipping fuels. The ERDF and the Innovation Fund can support projects including innovative clean and low-carbon technologies. EMSA provides industry with research on safety aspects associated with alternative

Like most sectors of the economy, maritime transport has been hit by the COVID-19 pandemic. As a result, the United Nations Conference on Trade and Development (UNCTAD) reported that the volume of imports and exports in Europe in 2020 diminished by 7.3% and 7.8%, compared to the previous year. However, in 2021, there was a rebound (8.3% and 7.9% on the previous year) due to the gradual reopening of economies.

Activities connected to freight transport were not, however, the ones hit the hardest due to the pandemic. Other economic activities of the sector suffered more, such as passenger transport, which was suspended in Europe in March 2020. In that period indeed, many countries implemented travel restrictions and lockdown measures to curb the spread of the virus, with harsh consequences on its economy.

![[Cargo vessel in the sea]](/sites/default/files/styles/embed_large/public/2022-04/AdobeStock_490522696.jpeg?itok=qVwESKz_)

The importance of maritime logistics for trade purposes has become very evident in 2022 due to the Russian invasion of Ukraine. With a reduced maritime connectivity and higher shipping costs, the inflation rose, so as shortages of food. This opens new trade scenarios for countries that try to substitute the supplier (e.g. Ukraine) that is unable to meet the demand. Looking ahead, the impact of the war impact on container shipping is likely to exacerbate due to a halt to the global economic growth and to reductions to consumer spending power. It will also increase oil prices, inflation, and the cost of living, and add economic and investor uncertainty.

Technological advancement, such as artificial intelligence, digitalisation and automation may rapidly change the way traditional maritime transport works and operates and can drive the growth of the sector. Development of (fully or partly) autonomous ships will pose both opportunities and challenges for the sector in terms of safety, security, existing legal frameworks, and operations. The Maritime Autonomous Surface Ships (MASS) have the potential to increase safety and productivity as well as to contribute towards the sustainability goals for maritime transport . Currently, autonomous and remote-controlled ships are being trialled in some sea areas and are expected to travel short distances in the near future.

Maritime transport remains an important pillar of the Blue Economy, playing a key role in the world’s economy and towards the achievement of EU decarbonisation objectives. Due to the expected growth of the world economy and associated transport demand from world trade, greenhouse gas emissions are projected to increase to 90-130% of 2008 emissions by 2050 for a range of plausible long-term economic and energy scenarios, according to the International Maritime Organization (IMO). These figures clash with the goal of climate neutrality, which requires a 90% reduction in transport emissions by 2050. Hence, more and cleaner transport alternatives are needed.

The European Commission outlines and revises environmental regulations and strategies to achieve the target of climate neutrality. The Sustainable and Smart Mobility Strategy sets out a path towards achieving the objectives of sustainable, smart and resilient mobility. The first important milestone is that zero-emission vessels will become ready for market by 2030. The FuelEU Maritime proposal outlines a framework to increase the share of renewable and low-carbon fuels in the fuel mix of international maritime transport, which currently relies entirely on fossil fuels.

The Commission also adopted an ambitious strategy for European transport under the umbrella of the European Green Deal. This new strategy is based on sustainability, built on multimodal transport systems (for both passengers and freight) enhanced recharging and refuelling infrastructure for zero emission vehicles, (including ships, boats, and ferries), and digitalisation and the use of new technologies. Delivering the establishment of wide-ranging ‘Emission Control Areas’ (ECAs) in all EU waters with zero pollution to air and water from shipping for the benefit of sea basins, coastal areas, and ports will be a priority. In particular, the Commission has spearheaded efforts to replicate the success of existing ECAs in areas of the Mediterranean Sea that require urgent protection. By 2030, such measures could cut emissions of SO2 and NOx from international shipping by 80% and 20%, compared to the current regulations. Similar efforts will also be made in the Black Sea region, where development is required.

Underwater noise from shipping is also increasingly recognised as a significant and pervasive pollutant, affecting marine ecosystems on a global scale. There is also documented scientific evidence linking noise exposure to a range of harmful effects on marine mammals, sea turtles, fish, and invertebrates. The impact affects species that are at serious risk of extinction, which are commercially important, and critical for supporting ecosystems. Under the marine strategy framework directive, EU experts have recently adopted recommendations on threshold values defining where and for how long marine habitats can be exposed to continuous underwater noise from shipping. To respect these limits, Member States have the responsibility to implement appropriate measures in their marine strategies, for example, by reducing ship-generated noise or setting spatial restrictions for human activity. At a global level, this also feeds ongoing discussions under the IMO to reduce the levels of underwater noise from shipping.

1 World Trade Organization - World Trade Statistical Review 2023

2 UNCTAD - Handbook of Statistics 2023

3 UNCTAD - Review of maritime transport 2023

4 UNCTAD - Handbook of Statistics 2023

5 EUROSTAT - Maritime transport statistics

6 EUROSTAT – Maritime passenger statistics

7 EUROSTAT – Maritime passenger statistics

8 Thai, V., Rahman, S., & Ma, S. (2023). Editorial: Post-COVID-19 global trade and business environment and maritime supply chain. Maritime Business Review.

9 UNCTAD. (n.d.). Red Sea, Black Sea and Panama Canal: UNCTAD raises alarm about disruptions to global trade. Retrieved from https://unctad.org/es/news/mar-rojo-mar-negro-y-canal-de-panama-la-unctad-alza-la-voz-de-alarma-sobre-las-perturbaciones

10 Transport and environment report 2022 Digitalization in the mobility system: challenges and opportunities

11 Global Marine Insurance Trends, IUMI 2023, https://iumi.com/statistics/public-statistics

12 DIRECTIVE (EU) 2023/959.

13 COM/2021/559

14 Mallouppas, G. and Yfantis, E.A., 2021. Decarbonization in shipping industry: A review of research, technology development, and innovation proposals. Journal of Marine Science and Engineering, 9(4), p.415.