The Marine non-living resources have been a significant sector of the EU Blue Economy for many years. Over the past decade, the mature offshore oil and gas sector has experienced a decline, following the ambitious EU decarbonisation goals and net-zero emission targets. However, there is potential for the sector to transition towards more sustainable practices, such as exploring and exploiting renewable energy sources, as well as contributing to the development and deployment of low-carbon technologies. Additionally, there is an increasing focus on oceanographic research and extracting raw materials from Europe's seas and oceans, which could play a crucial role in the transition to a sustainable Blue Economy. Therefore, while the traditional oil and gas sector may face challenges, there are opportunities for the industry to contribute to a more sustainable and environmentally friendly approach to extractive activities in EU waters.

The Marine non-living resources sector comprises two main subsectors:

- Oil and gas: Extraction of crude petroleum, Extraction of natural gas, Support activities;

- Other minerals: Operation of gravel and sand pits; mining of clays and kaolin; it also includes extraction of salt.

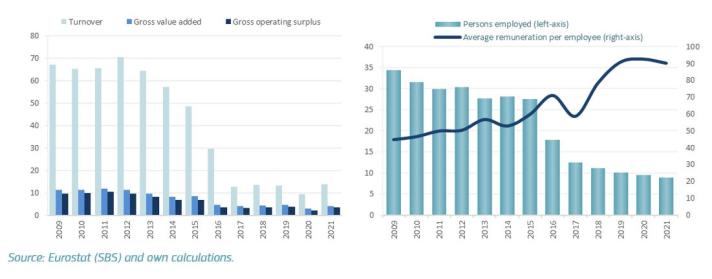

In 2021, the GVA generated by the sector amounted to €4.1 billion, up from €2.8 billion from the year earlier. This 46.5% increase, boosted by a similar year-on-year increase in turnover (+44.4%) – totalling €13.6 billion in 2021 – is a clear effect of the sharp increases in fuel prices following the Covid-19 pandemic. The sector’s good performance in 2021 is further testified by a 49.2% increase in profits, which reached €3.5 billion, up from €1.9 billion in 2020.

This notwithstanding, the oil and gas extractive sector kept shrinking, as testified by the continuous decrease in employment, which pursued the downward trend registered since 2009. In 2021, the Marine non-living resources sector employed more than 8,800 persons, i.e. nearly 600 less than in 2020 (slightly more than 9,400). The average annual remuneration per employee also decreased from €92,500 to €90,100 (-2.6%) (Figure 1).

Despite the 2021 rebound, the sector’s turnover fell sharply between 2012 and 2017, fluctuating between €10 and €13 billion, mainly because of fuel price dynamics. The sector’s workforce has been steadily declining since 2009, with only minor exceptions in 2012 and 2014. In 2021, the Marine non-living resources sector accounted for 9% of the jobs, 4% of the GVA and 3% of the profits of the entire EU Blue Economy.

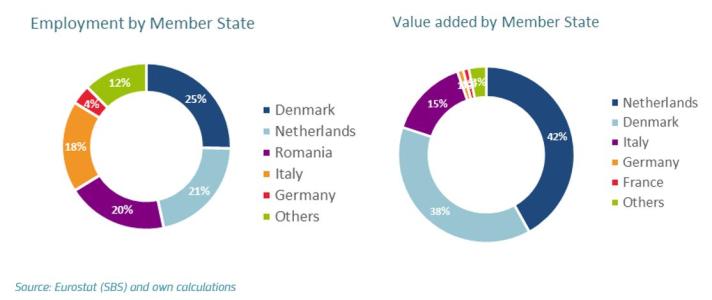

Denmark, Netherlands, Romania and Italy (in this order) lead the Marine non-living resources sector, employing 84% of the sectoral workforce. However, the Netherlands and Denmark together produce by far the largest share of the sector’s GVA (80%), followed by Italy (15%) (Figure 2).

Employment: The EU Marine non-living resources sector employed less than 9 thousand FTEs in 2021, compared to 34.3 thousand in 2009. The industry is among the most affected by the transition to sustainability in the energy sector, hence the strong decline in the workforce in line with global trends1. Despite its steady contraction, the Oil & gas sub-sector employed 84% of the sectoral, while people employed in operation and extraction of Other minerals amounted to the remaining 16%.

Gross value added: In 2021, the EU Marine non-living resources sector generated €4.1 billion in GVA, marking a 46.5% increase from 2020, mainly driven by rising fuel prices. The largest increase was registered in the Oil & gas sub-sector (99% of the year-on-year increase).

Production costs are rising due to the more expensive exploitation of deeper offshore fields and the use of non-conventional exploitation techniques – like fracking or tar sands. This is partly due to installations reaching their optimal design life of 25 years, which could be extended, but with rising operational costs. It is estimated that over 200 platforms and 2,500 wells will be in decommission phase by 2025 in the North Sea, the EU’s main oil &gas production area4. While costs are increasing, final prices are restraint to levels that ensure access of consumers and industries, limiting the adaptability of the industry and the need for alternative fuel sources5.

On the demand side, consumptionis being reduced due to the implementation of the ‘EU Fit for 55’ package, which prioritises the adoption of cleaner energy sources, and the REPowerEU measures, aimed at reducing energy dependence on Russia. Also, the transport industry, on which this sector heavily relies, is shifting towards greener solutions, which will further reduce demand on the coming years, in alignment with the International Maritime Organization (IMO) strategy to reduce maritime transport emissions to net-zero by around 2050.

On the supply side, there is intra-sectorial competition as oil-based fuels are being substituted partly by gas (LNG), which has reduced greenhouse gas emissions. The process involves liquefying natural gas at temperatures of -169ºC in dedicated facilities within the exporting nation. Subsequently, it is transported via tanker vessels, and later stored, degasified for integration into the gas network, or utilised as a fuel source. Additionally, traditional fuels are gradually replaced by newer, greener alternatives like e-methanol, e-ammonia, or biofuels. Furthermore, the sector is reliant on transport routes plagued by instability, like Russian pipelines or the Red Sea6.

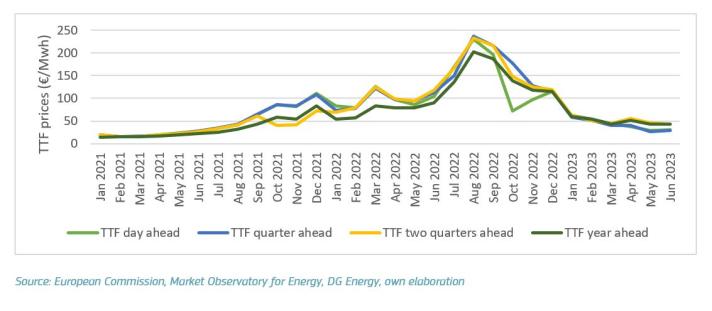

The prevailing trends in the sector are influenced by the repercussions of the Russian aggression against Ukraine and the subsequent sanctions imposed by the EU in response. The Russian decision to curtail or halt gas supply to European nations resulted in gas prices surging to unprecedented levels during the winter of 2022 (see Figure 3).

*Source: https://energy.ec.europa.eu/data-and-analysis/market-analysis_en#gas-ma…

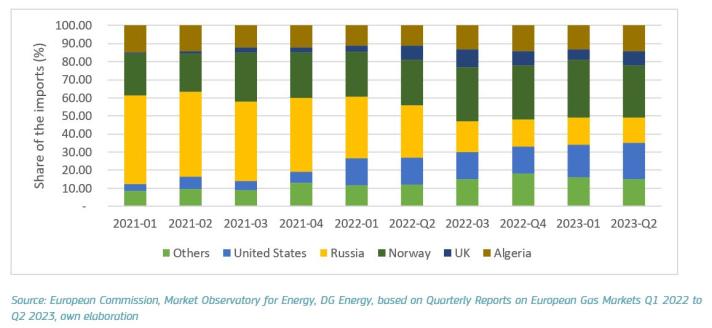

In response to the energy crisis, the EU has implemented measures focused on diminishing consumption, diversifying energy sources and reducing dependency on imports from specific countries. In this process, LNG emerged as a main solution facilitating the import of natural gas from countries lacking a direct pipeline connection. Notably, between 2021 and 2023, LNG imports within the EU experienced a noteworthy surge, escalating from 20% to 40% of total gas imports. This strategic shift has significant maritime implications, as the substitution of Russian pipeline gas is facilitated by the transport of LNG via ships and the use of maritime pipelines connecting with Norway and North African countries – the Mediterranean Hub.

The EU envisions the Mediterranean region as a pivotal source and route for supplying gas. The substantial potential of Algeria, coupled with the emergence of new gas reservoirs in the East Mediterranean and associated infrastructure development plans, enhances the region's role in EU energy diversification efforts. Notably, the Eastern Mediterranean region, featuring significant offshore gas reserves in Israel, Egypt, and Cyprus, emerges as a strategic partner for the EU in its pursuit of varied maritime gas supply routes. Options such as pipeline infrastructure and LNG projects, including the Cyprus East Med Pipeline and CyprusGas2EU LNG terminal designated as Projects of Common Interest, underscore the EU's commitment to fostering regional cooperation and energy security. The significant Connecting Europe Facility (CEF) grants awarded to the latter project in 2017 further underscore its strategic importance in advancing the EU's energy goals.

In addition to Norway and Algeria, other sources of increasing gas imports in the EU since 2021 are the United States and UK (Figure 4).

*Source: https://energy.ec.europa.eu/data-and-analysis/market-analysis_en#gas-mar

Particularly significant has been the rise in imports from the United States, increasing from 7% to 20% of the overall gas imports and reaching 50% of the EU's total LNG imports7, 8. This presents both challenges and opportunities for the EU gas production industry. While introducing a greater volume of gas and new competitors without direct pipeline, it foster greater diversification of EU gas supply.

Other important trends to be highlighted in the sectors include the rising trend of oil prices in the beginning of 2024, coming from the relative stability during the second semester of 2023. This results from halts in exports from OPEC countries, like the instability in the Red Sea – forcing tankers to avoid the Suez Canal in favour of the longer Cape of Good Hope – and an extreme Artic winter freeze in oil-producing North American regions9.

- Maritime transport and ports: These sectors play a key support role for the oil and gas industry. Not only are they responsible for the logistics of the sector, but they also provide maintenance, and will play a main role in decommissioning stages, requiring greater shore-based facilities. Oil and gas also impact these sectors by stablishing exclusion safety zones around their infrastructure and activity zones, impacting transport routes10. Also, LNG serves as a transition fuel for vessels, cleaner than diesel and meeting current IMO emission standards. While not a definitive solutions, it is helping alleviate carbon emissions while green fuels like e-methanol or e-ammonia reach technological and availability levels that allow their use for full-scale commercial operations.

- Pipelines and cables: the oil and gas industry is one of the main users of pipeline infrastructure. New extractive infrastructure and activities, also for other non-living resources, must consider existing pipelines and cables and ensure that they are not affected.

- Fishing: the extraction of non-living resources has a major impact on fishing activities. During operations and infrastructure decommissioning, fishing vessels must respect at minimum a 500 metres safety zone, with additional areas during the installation of pipelines. Also, operation activities can discharge contaminants in ecosystems, like crude or contaminated water, and the effect on noise and vibration is still under study11.

- Aquaculture: In spaces with available resources for both sectors, both activities are excluding. Co-location might be a future opportunity for these spaces, although technological and legal barriers must be first addressed, especially in the case of decommissioned structures.

- Offshore energy: While both sectors are competing for suitable space, there is potential for installation of offshore energies infrastructure in decommissioned structures, and possible synergies with operating ones, providing access to the electrical grid, and maintenance/logistical support.

- Conservation: The sector poses high ecological risks due to possible oil spills, ecological interactions during exploration, and noise pollution. Nevertheless, there is potential to provide protected spaces around the infrastructure, especially decommissioned structures, that can act as artificial reefs,

- Research and innovation: the sector is highly dependent upon new technologies that allow further exploitation of existing resources under controlled operational costs. It is estimated that around 50% of newly discovered deposits are in the deep-water (between 400 and 1,500 metres) and ultra-deep-water (more than 1,500 metres) range.

- Infrastructure and robotics: Robotics have high potential in the fields of exploitation and maintenance. Oil and gas deposits are exploring the development of subsea completion systems, deployed in the seabed, and managed by underwater robots. These systems are particularly beneficial for deep-water exploitation, as they reduce the need for offshore infrastructure, minimising environmental impacts and costs. Projects like the Chaintest, which received EU funding under the SME-FP6 programme, employ robots to reduce operational costs. For example, a robot that crawls along the chains anchoring platforms to the seabed, performing inspection and maintenance activities. Robotics also play a key part in the possible advance of seabed mining, providing selective and non-intrusive exploitation techniques. As an example of this, the EU funded ROBUST project advanced the development of an Autonomous Underwater Vehicle that can hover over the seabed, produce 3-D maps, and analyse resources, using laser technology.

1 ILO 2022. The future of work in the oil and gas industry.

2 EU Blue Economy Report 2023.

3 Marine Investment for the Blue Economy (MARIBE), WP 4: Socio-economic trends and EU policy in offshore Economy, https://maritime-spatial-planning.ec.europa.eu/media/12257

4 RAE 2013, Decommissioning in the North Sea, https://raeng.org.uk/media/b0ebnlfo/raeng_offshore_decommissioning_report.pdf.

5 Marine Investment for the Blue Economy (MARIBE), WP 4: Socio-economic trends and EU policy in offshore Economy, https://maritime-spatial-planning.ec.europa.eu/media/12257

6 S&P Global 2024, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/011724-european-oil-product-imports-fall-20-in-jan-on-red-sea-turmoil-cas

7 Quarterly Reports on European Gas Markets Q1 2022 to Q2 2023, Market Observatory for Energy, DG Energy, https://energy.ec.europa.eu/data-and-analysis/market-analysis_en#gas-market---recent-developments

8 Technical Study: MSP as a tool to support Blue Growth. Sector Fiche: Oil and Gas, Final Version: 16.02.2018, https://maritime-spatial-planning.ec.europa.eu/media/document/12243

9 IEA Oil Market Report - February 2024 https://www.iea.org/reports/oil-market-report-february-2024

10 Technical Study: MSP as a tool to support Blue Growth. Sector Fiche: Oil and Gas, Final Version: 16.02.2018, https://maritime-spatial-planning.ec.europa.eu/media/document/12243

11 Blue Growth Scenarios and drivers for Sustainable Growth from the Oceans, Seas and Coasts, 2012, https://maritime-forum.ec.europa.eu/document/download/dd6e0bfd-bd35-44f4-9a44-603190abbd31_en?filename=Blue%20Growth%20Final%20Report%2013092012.pdf